bigredfish

Known around here

Hmmmm Portland, Chicago, San Francisco … I’m thinking they have something in common..

Last edited:

You caught me. I've lived in or near all of them. I do my destruction then move on to the next target, while gaslighting the public into thinking the dems are responsible.Hmmmm Portland, Chicago, San Fransisco … I’m thinking they have something in common..

Soros-Funded St Louis Circuit Attorney Kim Gardner’s Office No-Shows Murder Trial Allowing Killer to Walk Free * The Gateway Pundit * by Joe Hoft

There's something very, very wrong with this individual who is allowed to destroy the rule of law in St.www.thegatewaypundit.com

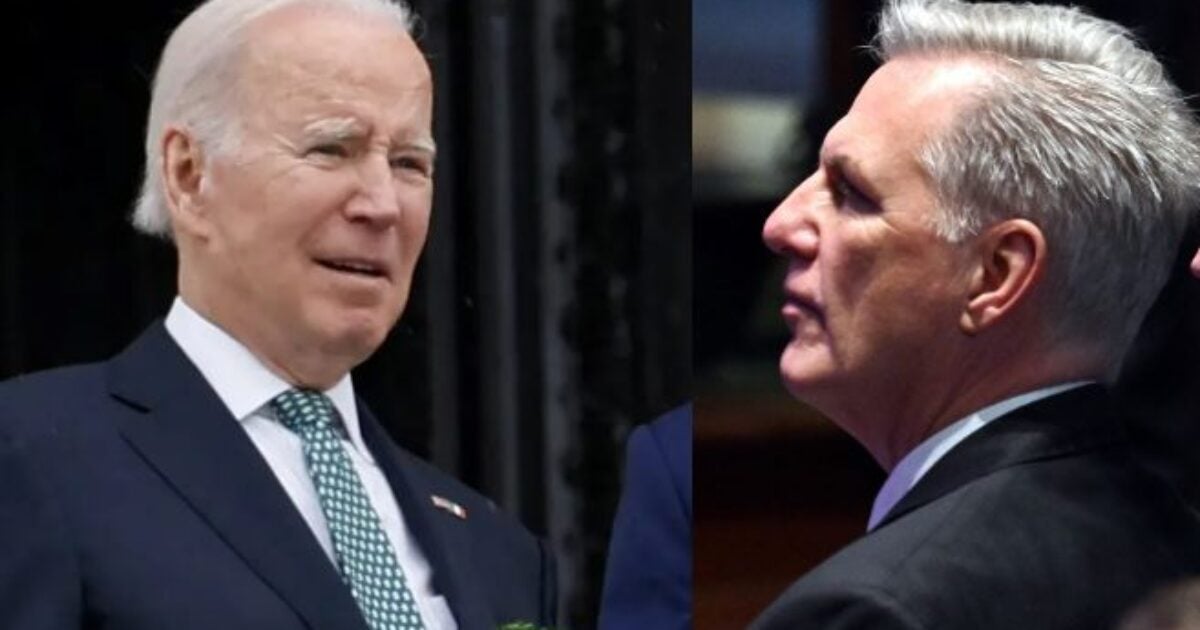

Huh? What kind of double speak is this?? Increase debt limit and cut spending??? Rainbows and Unicorns...

Speaker McCarthy Says the House GOP Will Increase the Debt Limit and Cut Spending * The Gateway Pundit * by Joe Hoft

Speaker McCarthy agrees to increase the debt ceiling till 2024 but he's going to cut spending at the same time. The House GOP says that it raised the debt…

The sad part is, something north of 50% of the population will believe that. We now live in a country where one of every two people you meet are complete fucking morons and are just taking up otherwise perfectly good oxygen.

The sad part is, something north of 50% of the population will believe that. We now live in a country where one of every two people you meet are complete fucking morons and are just taking up otherwise perfectly good oxygen.

rumble.com

rumble.com

")

The new fees “will create extreme confusion as we enter the traditional spring home purchase season,” said David Stevens, a former head of the Mortgage Bankers Association who served as commissioner of the Federal Housing Administration during the Obama administration.

“This confusing approach won’t work and more importantly couldn’t come at a worse time for an industry struggling to get back on its feet after these past 12 months,” Mr. Stevens wrote in a recent social media post. “To do this at the onset of the spring market is almost offensive to the market, consumers, and lenders.”

The housing market has been hit hard by a series of Federal Reserve interest rate hikes that have driven mortgage rates above 6%, roughly double the level from early 2022. The Fed has raised rates rapidly to bring down inflation, which hit a four-decade high of 9.1% last summer. -Washington Times